Should I take Return of Premium option in Term Insurance?

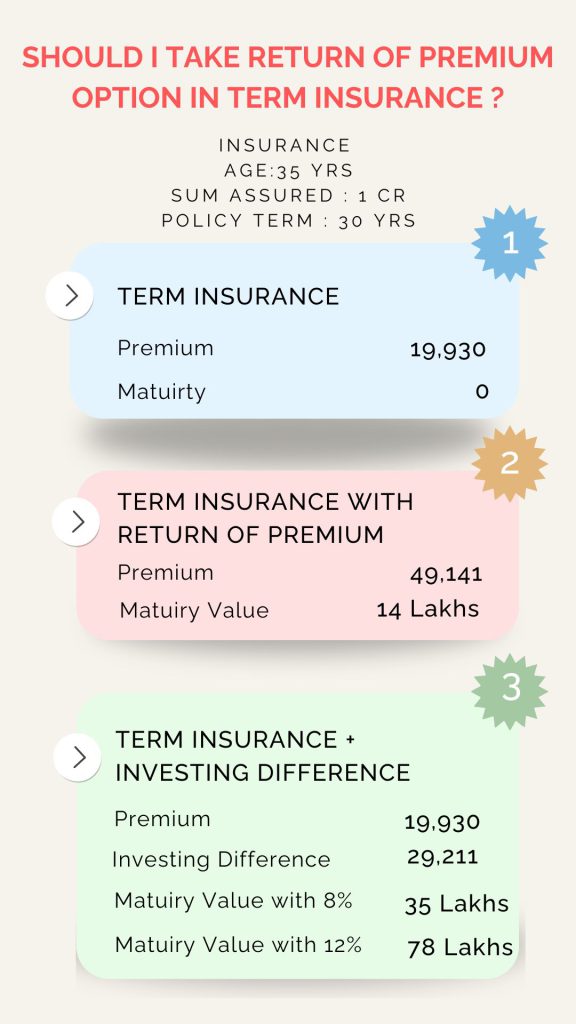

Comparison of Term Insurance Options for a 35-Year-Old Person

| Option | Annual Premium (₹) | Maturity Value (₹) | Extra Investment Opportunity (₹) | Potential Additional Wealth (₹) |

|---|---|---|---|---|

| 1. Pure Term Insurance | 19,930 | 0 | 29,211 | – |

| 2. Term Insurance with Return of Premium (TROP) | 49,141 | 14,74,230 | 0 | 0 |

| 3. Term Insurance + Investing Difference at 8% | 19,930 + 29,211 | 14,74,230 + 35,73,845 | – | +20,99,615 |

| 4. Term Insurance + Investing Difference at 12% | 19,930 + 29,211 | 14,74,230 + 78,95,517 | – | +64,21,287 |

Advantages & Comparison

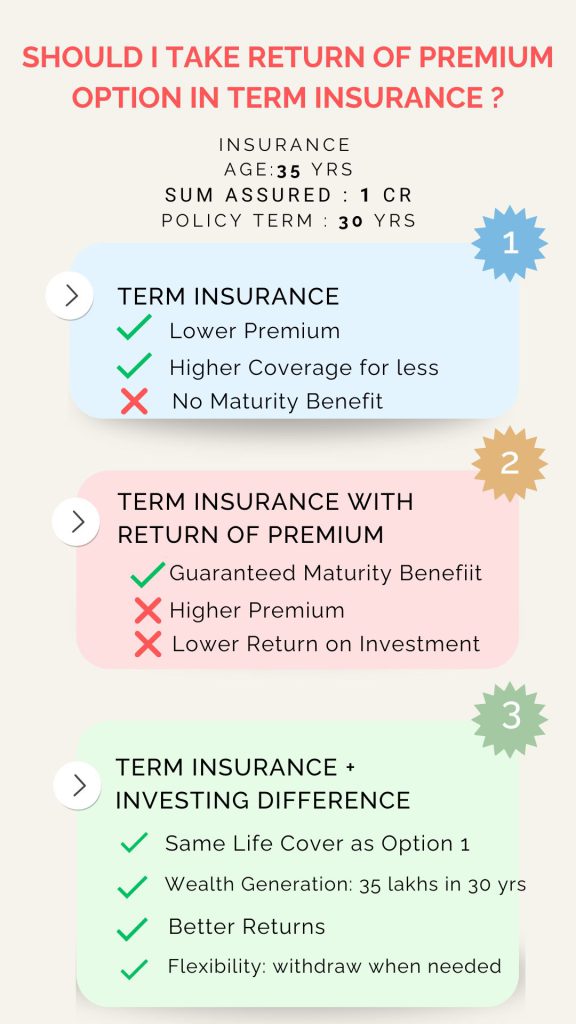

1. Pure Term Insurance (Option 1)

- ✅ Lower Premium: ₹19,930 per year, ensuring affordability.

- ✅ Higher Coverage for Less: The primary objective of term insurance is protection. This option provides a ₹1 crore life cover at the lowest cost.

- ❌ No Maturity Benefit: If the insured survives the term, there is no return of premiums.

2. Term Insurance with Return of Premium (TROP) (Option 2)

- ✅ Guaranteed Maturity Benefit: If the policyholder survives, they get ₹14,74,230 back.

- ❌ Higher Premium: ₹49,141 per year, which is 2.47x the cost of pure term insurance.

- ❌ Lower Return on Investment: The effective return on premium (₹14,74,230) is very low compared to what the additional premium could earn elsewhere.

3. Term Insurance + Investing the Difference at 8% (Option 3)

- ✅ Same Life Cover as Option 1: ₹1 crore coverage.

- ✅ Wealth Generation: If the additional ₹29,211 is invested at 8% annually, it can generate ₹35,73,845 in 30 years.

- ✅ Better Returns than TROP: Compared to the TROP’s maturity amount, this generates an additional ₹20,99,615.

4. Term Insurance + Investing the Difference at 12% (Option 4)

- ✅ Highest Wealth Growth: Investing the difference at 12% results in ₹78,95,517 in 30 years.

- ✅ Maximum Additional Wealth: Compared to TROP, this option generates ₹64,21,287 extra.

- ✅ Flexibility: Unlike TROP, investments can be liquid, allowing withdrawals when needed.

Final Conclusion: Which is the Best?

- TROP (Option 2) is a poor choice because the returns are significantly lower than what can be achieved by investing the difference separately.

- Pure Term Insurance + Investing the Difference (Option 3 or 4) is superior, especially if one can achieve returns of 8% or 12%.

- Higher returns mean massive wealth creation: With 12% returns, you can generate over ₹64 lakhs more than the TROP option.

Thus, Option 4 (Pure Term Insurance + Investing Difference at 12%) is the best strategy for maximizing financial benefits.